Contract subrogation is a legal principle that allows one party to step into the shoes of another to claim their rights, typically in cases involving insurance, debt repayment, or contractual disputes. Subrogation plays a crucial role in various types of contracts, particularly in insurance and financial agreements, ensuring that parties receive due compensation and that the responsible entities bear the appropriate costs. Understanding subrogation is vital for businesses, insurance companies, and individuals as it helps clarify who is ultimately responsible for losses and ensures that the proper parties are compensated.

In this article, we will explore the concept of contract subrogation in detail, discuss its different types, delve into the key clauses involved, examine real-world examples, and answer common questions surrounding this principle.

What is Contract Subrogation?

Subrogation is the process by which one party (typically an insurer) assumes the legal rights of another party (such as an insured individual) to recover costs from a third party responsible for causing a loss. In other words, subrogation allows the insurer to “step into the shoes” of the insured and seek compensation from the party responsible for the damages. This principle is vital in maintaining fairness in contractual relationships and ensuring that losses are borne by those who are ultimately responsible.

For example, if you have an auto insurance policy and your car is damaged in an accident caused by another driver, your insurance company may cover the repair costs initially. Through subrogation, the insurer will then seek reimbursement from the at-fault driver’s insurance company.

Read More: How to Write a Contract

The Legal Basis for Subrogation

Subrogation has its roots in both contract law and equity. The legal principle of subrogation is typically embedded in contracts, such as insurance policies, where the insurer is granted the right to pursue recovery against third parties. However, subrogation can also arise under equitable doctrines, where courts allow one party to pursue another’s rights to prevent unjust enrichment or unfair loss allocation.

There are three primary forms of subrogation recognized by law:

- Contractual Subrogation: This form is established through an agreement between parties, often specified in insurance policies, indemnity agreements, or other contracts. Here, one party explicitly transfers their right to recover from a third party to another.

- Equitable Subrogation: In cases where there is no express agreement, equitable subrogation allows one party (e.g., an insurer) to pursue claims against a third party based on fairness and preventing unjust enrichment.

- Statutory Subrogation: Certain laws and regulations may automatically grant subrogation rights to insurers or other parties, providing a legal framework for recovering costs.

Read More: Understanding Contract Termination

Types of Contracts Involving Subrogation

Subrogation is most commonly encountered in insurance contracts, but it can also arise in other types of agreements, including:

- Insurance Contracts: Subrogation is a standard clause in most insurance policies, allowing insurers to recover costs from third parties responsible for losses covered under the policy.

- Indemnity Agreements: In indemnity contracts, the party providing indemnity may be subrogated to the rights of the indemnified party to seek recovery from responsible third parties.

- Debt Repayment Contracts: Lenders and creditors may utilize subrogation to recover unpaid debts from third parties responsible for the debtor’s financial difficulties.

- Construction Contracts: In the construction industry, subrogation clauses may apply when contractors, subcontractors, or suppliers cause damage, allowing the injured party’s insurer to pursue recovery from the responsible party.

Read More: What is a Contract Clause?

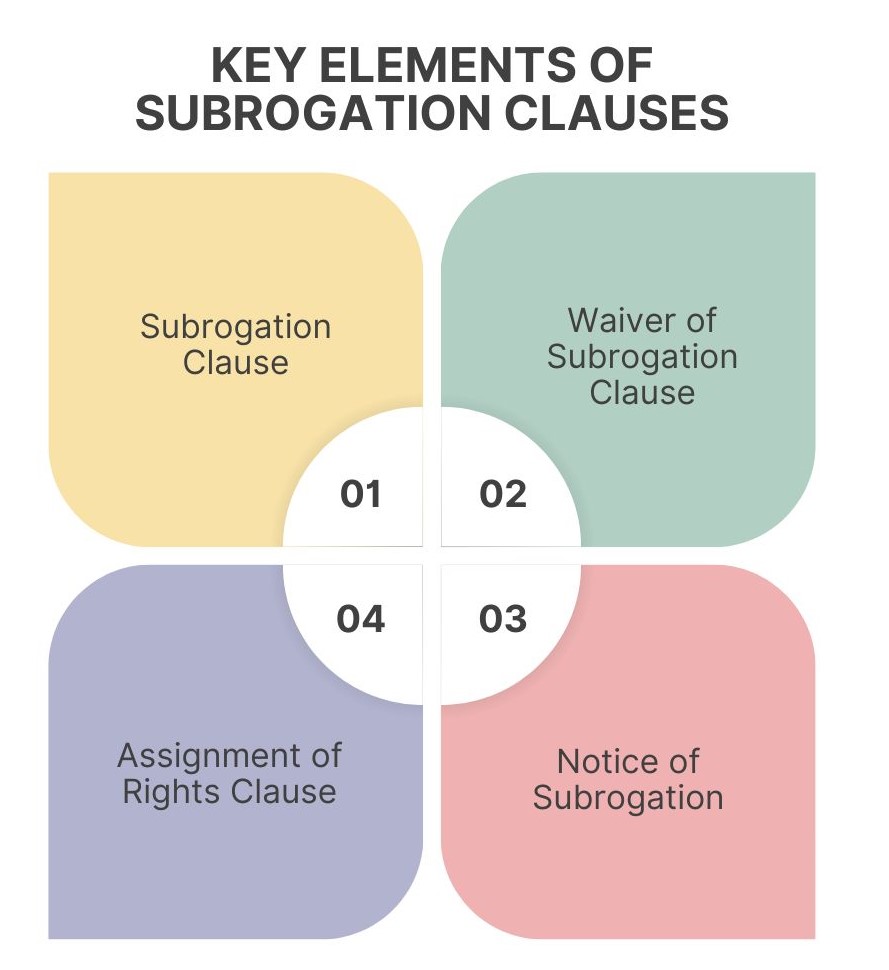

Key Clauses in Subrogation Agreements

Understanding the language in subrogation clauses is critical to ensuring proper enforcement of subrogation rights. The following are some common clauses found in contracts related to subrogation:

- Subrogation Clause: This is the core provision that explicitly grants subrogation rights to the insurer or indemnifying party. It typically states that the insurer, upon paying for a loss, is entitled to pursue recovery from any third party responsible for the damages.

- Waiver of Subrogation Clause: This clause limits the subrogation rights of an insurer or indemnitor. Parties to a contract may agree to waive subrogation to prevent one party from being pursued by the other’s insurer. Waivers are often found in construction contracts to maintain good working relationships between contractors and subcontractors.

- Notice of Subrogation: Some contracts require the insured or indemnified party to provide notice of any claims or third-party recovery actions. Failing to notify the insurer could limit or void subrogation rights.

- Assignment of Rights Clause: This provision assigns the right to pursue claims to another party (usually the insurer). It is important to note that assignment of rights is different from subrogation in that assignment transfers full ownership of the claim, whereas subrogation only transfers the right to recovery.

How Subrogation Works in Practice

Subrogation typically follows a structured process in contractual relationships, particularly in insurance claims. Below is a general overview of how subrogation works in an insurance context:

- Filing the Claim: The insured party files a claim with their insurer for damages caused by a third party (e.g., an auto accident caused by another driver). The insurer evaluates the claim and determines coverage under the policy.

- Payment of the Claim: If the claim is covered, the insurer compensates the insured party for the damages or losses, effectively assuming financial responsibility for the claim.

- Investigation and Pursuit: Once the insurer has paid the claim, it investigates the circumstances to determine if a third party is responsible. If so, the insurer exercises its subrogation rights and seeks recovery from the third party or their insurance company.

- Recovery of Costs: If successful, the insurer recovers its costs from the responsible party, which may include legal fees, claim payments, and any other expenses incurred during the claim process.

- Reimbursement of Deductibles: In cases where subrogation is successful, the insured party may be entitled to a reimbursement of their deductible.

Examples of Subrogation

To better understand subrogation, let’s explore some real-world examples across various industries:

Example 1: Automobile Insurance Subrogation

John is driving his car when he is rear-ended by another driver, Lisa. John files a claim with his auto insurance company, which pays for the repairs. Because Lisa is at fault for the accident, John’s insurer has the right to subrogate against Lisa’s insurer to recover the amount paid for the repairs.

Example 2: Health Insurance Subrogation

Sarah is injured in a workplace accident caused by faulty equipment. She receives treatment, and her health insurance covers the medical bills. Her insurer then subrogates against the manufacturer of the faulty equipment to recover the costs of her treatment.

Example 3: Property Insurance Subrogation

A tenant accidentally starts a fire in their rented apartment, causing significant damage. The landlord’s property insurance covers the repair costs, but the insurer subrogates against the tenant to recover the costs, as the tenant was responsible for the fire.

Example 4: Indemnity Agreement Subrogation

A construction subcontractor damages a building during renovations. The contractor, who is indemnified under a contract, seeks compensation from their indemnity insurer. The insurer, after paying the contractor, subrogates against the subcontractor to recover the repair costs.

Challenges and Limitations of Subrogation

While subrogation is a powerful legal tool, it is not without its challenges and limitations. Some common issues that arise in subrogation cases include:

- Waivers of Subrogation: Many contracts include waivers of subrogation, which prevent the insurer from pursuing third parties. This can complicate recovery efforts, particularly in industries like construction where such waivers are common.

- Statutory Limitations: Some jurisdictions impose statutory limits on subrogation rights, particularly in the context of workers’ compensation and health insurance. Insurers must navigate these legal frameworks to successfully pursue recovery.

- Third-Party Bankruptcy: If the responsible third party is bankrupt or insolvent, recovering costs through subrogation may be impossible, leaving the insurer to absorb the loss.

- Timing of Recovery: Subrogation can be a lengthy process, particularly when litigation is involved. Insurers and insured parties may face delays in recovering funds, which can impact financial planning.

- Disputes Over Fault: In many subrogation cases, determining who is at fault is a key issue. If fault is contested, the subrogation process may involve lengthy negotiations or legal proceedings.

Importance of Subrogation in Contract Law

Subrogation is essential in contract law because it ensures that losses are appropriately allocated to the responsible parties. Without subrogation, insured parties might be forced to bear the costs of losses caused by others, while responsible third parties would avoid liability. Subrogation also helps insurers mitigate their losses by pursuing recovery from at-fault parties, reducing the overall cost of claims.

In industries like insurance, finance, and construction, subrogation clauses and procedures are fundamental in managing risk and ensuring that the proper parties are held accountable for damages. Businesses, insurers, and legal professionals must carefully review contracts to understand the subrogation rights and responsibilities of each party.

Read More: How to Draft a Simple Contract

Conclusion

Contract subrogation is a vital concept in the world of insurance, indemnity, and other contractual relationships. By allowing one party to step into the shoes of another, subrogation ensures that losses are properly allocated and that responsible parties are held accountable. Whether through contractual agreements, statutory provisions, or equitable principles, subrogation helps maintain fairness in legal and financial relationships.

Understanding the intricacies of subrogation is crucial for businesses, insurers, and individuals alike. Clear contract language, careful management of claims, and a thorough knowledge of legal frameworks can help prevent disputes and ensure successful recovery through subrogation.

In conclusion, contract subrogation plays a critical role in balancing the rights and responsibilities of all parties involved in a contract, and its importance cannot be overstated in industries that regularly deal with risk and compensation.

Did you find this article worthwhile? More engaging blogs and products about smart contracts on the blockchain, contract management software, and electronic signatures can be found in the Legitt AI. You may also contact Legitt to hire the best contract lifecycle management services and solutions, along with free contract templates.

FAQs on Contract subrogation

What is contract subrogation?

Contract subrogation is a legal process that allows one party, usually an insurer, to assume the rights of another party, such as the insured, to recover costs from a third party responsible for causing a loss. The insurer steps into the shoes of the insured to seek reimbursement from the at-fault party.

How does subrogation work in insurance contracts?

In an insurance contract, subrogation occurs when the insurer pays a claim to the insured for damages or losses caused by a third party. The insurer then pursues recovery from the responsible third party or their insurer to recoup the costs of the claim. The insured assigns their right to recover damages to the insurer.

What is the difference between subrogation and assignment of rights?

Subrogation allows one party (e.g., an insurer) to step into the shoes of another (e.g., the insured) to pursue recovery, but it does not transfer ownership of the claim. Assignment of rights, on the other hand, transfers full ownership of the claim to another party, who can then pursue it as if it were their own.

Can subrogation be waived in a contract?

Yes, subrogation can be waived in a contract through a waiver of subrogation clause. This clause prevents one party’s insurer from pursuing the other party for damages, often to maintain good business relationships. Such clauses are common in industries like construction.

What types of contracts commonly involve subrogation?

Subrogation is most commonly found in insurance contracts (e.g., auto, health, and property insurance), but it also appears in indemnity agreements, debt repayment contracts, and construction contracts, where parties seek to recover costs from third parties responsible for damages.

What are the challenges in enforcing subrogation rights?

Challenges in enforcing subrogation rights include waivers of subrogation clauses, statutory limitations, disputes over who is at fault, third-party bankruptcy or insolvency, and delays caused by litigation. These factors can complicate or delay the recovery process for insurers.

What is equitable subrogation?

Equitable subrogation is a principle that allows one party to assume another’s legal rights to pursue recovery based on fairness, even if there is no express contract. Courts apply equitable subrogation to prevent unjust enrichment or unfair allocation of losses.

Can subrogation impact the insured party?

Subrogation can benefit the insured party because, if successful, the insured may be reimbursed for any deductible they paid. However, the insured must cooperate with the insurer during the subrogation process to ensure the insurer can successfully recover costs from the responsible third party.

Is subrogation always available in all types of insurance claims?

No, subrogation is not available in all insurance claims. Certain jurisdictions may impose statutory limitations on subrogation rights in specific types of claims, such as workers’ compensation or health insurance. Additionally, if a waiver of subrogation exists in the contract, the insurer may not have the right to pursue recovery.

What happens if the responsible third party cannot pay in subrogation?

If the responsible third party is bankrupt, insolvent, or otherwise unable to pay, the insurer may not be able to recover the costs through subrogation. In this case, the insurer typically absorbs the loss, and the insured may not be reimbursed for their deductible, depending on the terms of the insurance policy.