In business and contracting, different pricing models can be used in managing projects and services. The Fixed-Price Contract is one of the most widely-used models. Knowing how this type of contract works will help businesses and contractors effectively manage expectations, budgets, and project outcomes. This guide will help you understand everything about Fixed-Price Contracts, whether you are a contractor, business owner, or project manager.

What Is a Fixed-Price Contract?

A Fixed-Price Contract, sometimes referred to as a lump-sum contract, is a legally binding agreement in which the payment amount for a project or service is set at a predetermined fixed rate. Unlike other types of contracts, this pricing model does not change based on the actual time or resources spent on the project.

Fixed-Price Contracts are often used in construction, IT services, and manufacturing, where the scope of work is well-defined. Since the price is fixed, both parties can predict costs and risks more accurately.

Key Characteristics of a Fixed-Price Contract

A Fixed-Price Contract is a structured agreement where the price is set in advance for a clearly defined project. Below are its key characteristics explained in detail:

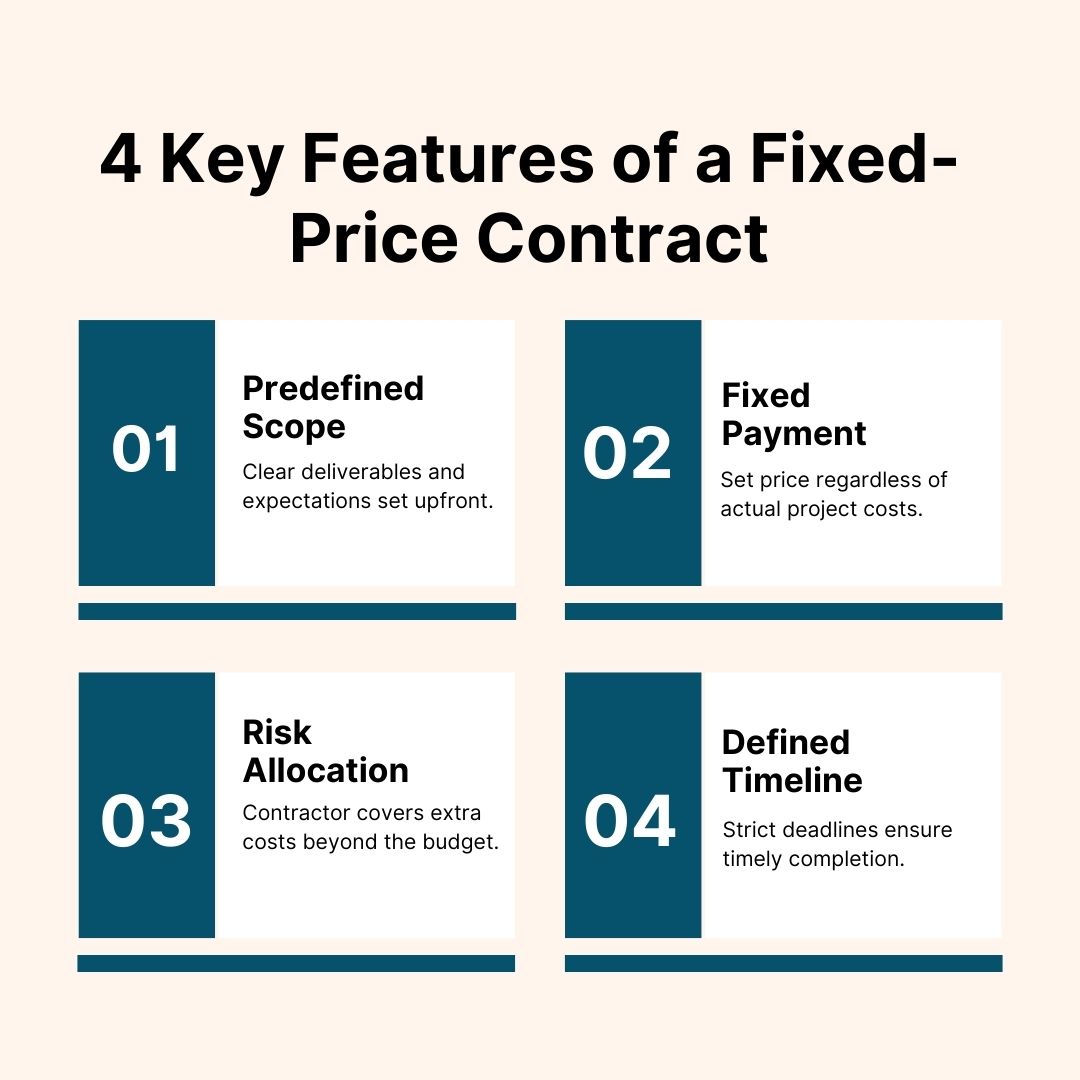

1. Predefined Scope: The scope of work is thoroughly defined and documented before the project begins. Both parties agree on deliverables, specifications, and expectations, minimizing ambiguity and ensuring the contractor and client are on the same page.

2. Fixed Payment: The contractor is paid a predetermined amount, regardless of the actual costs incurred during the project. This provides the client with financial predictability while motivating the contractor to manage costs effectively.

3. Risk Allocation: The contractor assumes most of the financial risk. If costs exceed estimates due to unforeseen issues, the contractor is responsible for covering the additional expenses without adjusting the agreed price.

4. Defined Timeline: Fixed-Price Contracts often include strict deadlines or milestone schedules. These timelines are crucial for monitoring progress and ensuring the project is delivered on time without compromising quality or budget.

Types of Fixed-Price Contracts

Fixed-Price Contracts come in various forms, each designed to address specific project needs and circumstances. Below is a comprehensive explanation of the most common types:

1. Firm Fixed-Price Contract (FFP)

This is the simplest and most straightforward type of Fixed-Price Contract. The total contract amount is determined at the beginning and remains unchanged, regardless of any changes in circumstances or project costs. The contractor is responsible for managing costs, which can lead to higher profits if they stay within budget but also poses a risk if expenses exceed expectations.

2. Fixed-Price Incentive Fee (FPIF)

In this type of contract, the contractor has an opportunity to earn an additional incentive fee for meeting or exceeding specified performance objectives. These objectives could include completing the project ahead of schedule or delivering the work at a reduced cost while maintaining quality. This arrangement encourages efficiency and innovation, as the contractor is rewarded for optimal performance.

3. Fixed-Price with Economic Price Adjustment (FPEPA)

This contract offers some flexibility for long-term projects that are subject to external economic factors. Adjustments are made based on predefined conditions such as changes in inflation, labor costs, or raw material prices. This helps both parties manage risks related to market fluctuations while ensuring fairness in pricing over time.

4. Fixed-Price Level of Effort (FPLOE)

This type of contract is used when the work cannot be easily quantified in terms of deliverables but requires a certain level of effort for a specified time. Payment is based on the number of hours or days worked at a fixed rate, making it ideal for research and development projects or consulting services.

5. Fixed-Price Award Fee (FPAF)

In this variation, the contractor is eligible for an award fee based on subjective evaluation of their performance, including quality of work, customer satisfaction, and adherence to deadlines. The fee is not guaranteed and is only awarded at the discretion of the client, which motivates the contractor to exceed expectations.

6. Fixed-Price with Prospective Price Redetermination

This contract sets an initial fixed price for an early phase of the project, with provisions to renegotiate the price for later phases based on actual costs and performance data. This type is useful for long-term projects where costs are difficult to predict at the start.

7. Fixed-Price with Successive Targets

In this contract, an initial target price is set, followed by successive adjustments as more details about the project become available. This approach provides a balance between cost control and flexibility, allowing adjustments based on actual progress and cost data.

8. Fixed-Price Time and Materials Hybrid

A hybrid between Fixed-Price and Time and Materials contracts, this type combines elements of both. While the overall price is capped, certain portions of the work—such as maintenance or additional support—are billed based on actual time and materials used within agreed parameters.

Benefits of a Fixed-Price Contract

Using a Fixed-Price Contract offers significant advantages for both buyers and contractors. It creates a predictable, structured agreement that reduces financial uncertainty and encourages project efficiency. Here’s a detailed breakdown:

For Buyers

1. Predictable Costs

One of the primary benefits for buyers is the certainty of project costs. Since the price is agreed upon upfront, there are no unexpected financial surprises. This makes it easier to plan budgets and manage resources without worrying about fluctuating expenses throughout the project.

2. Reduced Risk

The buyer’s financial risk is significantly minimized. In a Fixed-Price Contract, the contractor is responsible for absorbing any cost overruns due to unforeseen circumstances or miscalculations. This provides peace of mind and greater control over financial exposure.

3. Clear Expectations and Deliverables

Fixed-Price Contracts promote clarity from the outset by clearly defining the project scope, deliverables, and deadlines. This reduces ambiguity, minimizes misunderstandings, and helps align the buyer and contractor on shared goals. A well-defined agreement ensures that the buyer knows exactly what to expect and when.

For Contractors

1. Incentive for Efficiency and Profitability

A Fixed-Price Contract incentivizes contractors to work efficiently. Since the payment is fixed regardless of actual costs, contractors can increase profitability by optimizing resource use, managing expenses effectively, and completing the project on time or ahead of schedule. Efficient project management directly translates into higher earnings.

2. Simpler Payment Structure

Fixed-Price Contracts often come with a milestone-based payment structure. This means contractors receive payments at predefined stages of project completion, ensuring a steady and predictable cash flow. This structure simplifies invoicing and financial planning, allowing contractors to focus more on project delivery.

Drawbacks of a Fixed-Price Contract

While Fixed-Price Contracts provide stability and predictability, they also come with certain challenges for both buyers and contractors. It’s important to understand these drawbacks to manage expectations and mitigate risks effectively.

For Buyers

1. Higher Initial Cost

To protect themselves from potential risks, contractors often add a contingency or risk premium to the fixed price. This can result in higher upfront costs compared to other contract types. While this ensures the contractor won’t suffer losses, buyers may end up paying more than necessary if the project proceeds smoothly without any surprises.

2. Limited Flexibility

Once a Fixed-Price Contract is signed, making changes to the project scope can be both costly and complicated. Any modifications typically require a formal change order, which can delay the project and increase costs. This rigid structure makes it less suitable for projects where requirements might evolve over time.

For Contractors

1. Increased Risk Exposure

In Fixed-Price Contracts, the contractor assumes full responsibility for managing costs and meeting deadlines. If unforeseen circumstances arise—such as delays, price fluctuations in materials, or changes in labor availability—the contractor absorbs the associated expenses. This increased risk can put significant pressure on project planning and execution.

2. Potential Profit Loss

Estimating project costs accurately is crucial in Fixed-Price Contracts. If the contractor underestimates the required resources, labor, or time, it can quickly lead to financial losses. Unlike time-and-materials contracts, there’s no opportunity to recoup additional costs, which can hurt profitability and, in extreme cases, lead to project failure.

When to Use a Fixed-Price Contract

A Fixed-Price Contract is highly effective when the project scope, budget, and timeline are clearly defined and agreed upon. It’s an excellent choice for projects with predictable outcomes, where risks can be managed and changes are minimal. Here are some common situations where it’s the best option:

1. Construction Projects

Fixed-Price Contracts are widely used in the construction industry, especially for new builds with detailed architectural plans and engineering specifications. These contracts ensure cost predictability for both parties and help maintain strict control over the budget and timeline. Since construction projects often involve well-defined deliverables, this contract type is a natural fit.

2. Product Development

When developing a specific product with minimal expected changes, a Fixed-Price Contract can streamline the process. This approach works well when the project requirements are thoroughly documented upfront, allowing both parties to agree on the cost and timeline in advance. It reduces the need for ongoing negotiations and helps keep the focus on delivery.

3. Government Contracts

Government agencies frequently use Fixed-Price Contracts to maintain cost predictability and accountability. These contracts ensure that taxpayer funds are spent efficiently, and they reduce the potential for unexpected budget increases. The rigid structure makes them ideal for large-scale federal projects with clear objectives and minimal scope for change.

4. Event Planning

For events with a defined budget, timeline, and scope—such as corporate conferences or weddings—a Fixed-Price Contract offers clarity and financial security. The event planner and client agree on the cost and deliverables upfront, minimizing surprises and ensuring the event is executed as planned.

When Not to Use a Fixed-Price Contract

While Fixed-Price Contracts offer numerous advantages, they may not be suitable for all types of projects. Here are some instances where it’s better to explore alternative contract structures:

1. Evolving Projects

For projects with uncertain or frequently changing requirements, a Fixed-Price Contract can become restrictive and costly. Every modification requires a change order, which can slow progress and increase expenses. Flexible contract types, such as time-and-materials or cost-plus contracts, are often better suited for evolving projects where adaptability is key.

2. High-Risk Initiatives

Projects that involve significant uncertainty or a high likelihood of unforeseen expenses are not ideal for Fixed-Price Contracts. Examples include research and development projects or innovative initiatives with many unknown factors. The fixed cost can quickly become inadequate, leading to disputes or financial losses for one or both parties.

Steps to Create a Fixed-Price Contract

Drafting a Fixed-Price Contract requires careful planning and attention to detail. Clear communication and thorough documentation are essential to ensure that both parties understand the terms and expectations. Follow these steps to create a well-structured, enforceable Fixed-Price Contract.

Step 1: Define the Scope of Work

The first step in creating a Fixed-Price Contract is to clearly define the scope of work. This involves detailing all the tasks, deliverables, and deadlines associated with the project. A well-defined scope ensures that both parties have a shared understanding of what is expected and helps avoid ambiguity. Be specific about the work to be performed, including any special requirements or standards that need to be met. A comprehensive scope helps prevent disputes and ensures that the project progresses smoothly.

Step 2: Set a Fixed Price

The next step is to determine the total price for the project. This is typically based on a detailed estimate of the costs involved, including labor, materials, and any other resources required. It’s important to be realistic in your pricing and to factor in potential risks. A risk assessment should also be included to account for unforeseen circumstances such as price increases or delays. Setting the right price is crucial, as underestimating the cost can lead to financial losses or disputes later on.

Step 3: Establish Milestones and Payment Terms

In a Fixed-Price Contract, payments are usually made at specific milestones or project phases. Break down the project into manageable stages and assign a payment schedule for each phase. This helps ensure that both parties remain aligned throughout the project, and the contractor receives payment for completed work. The payment terms should be clearly stated, indicating when payments are due and how they will be processed. This step promotes transparency and ensures that there are no misunderstandings regarding financial obligations.

Step 4: Include Risk and Liability Clauses

Every project carries some level of risk, and a Fixed-Price Contract should address this. Clearly outline who is responsible for various risks, such as delays, cost overruns, or unforeseen events. Establishing these terms in advance helps both parties understand their obligations in case of issues that may arise during the project. Risk and liability clauses should define what happens if the contractor fails to deliver on time or if costs exceed the agreed price.

Step 5: Add Terms for Changes and Disputes

Although a Fixed-Price Contract is typically rigid in terms of scope and cost, changes can still occur. It’s important to include provisions that outline how changes to the project will be handled. Define the process for requesting and approving changes, as well as any associated costs. Additionally, include a clause for resolving disputes, should they arise. This provides a clear process for handling disagreements, helping to avoid delays and potential litigation.

These steps are designed to help you create a Fixed-Price Contract that is thorough, fair, and legally sound. By being clear about expectations, pricing, and responsibilities, you can ensure that both parties are satisfied with the agreement and reduce the risk of disputes during the course of the project.

How Legitt AI Can Help

Drafting, managing, and reviewing Fixed-Price Contracts can be complex and time-consuming. This is where Legitt AI comes in. Legitt AI simplifies contract management by providing advanced features for contract creation, automated reviews, and compliance checks.

Key Benefits of Legitt AI for Fixed-Price Contracts

- Automated Drafting: Quickly generate Fixed-Price Contracts using customizable templates.

- AI-Powered Review: Ensure the contract is free from errors and compliant with legal standards.

- Risk Analysis: Identify potential risks and gaps in the contract before signing.

By leveraging Legitt AI, businesses can reduce the risk of costly mistakes and streamline their contract processes.

Conclusion

A Fixed-Price Contract is a powerful tool for managing projects with a clearly defined scope and budget. While it offers predictability and simplicity, it also requires careful planning and risk management. By understanding the types, benefits, and drawbacks of Fixed-Price Contracts, you can make informed decisions and protect your business interests.

Whether you’re drafting your first Fixed-Price Contract or refining an existing one, tools like Legitt AI can help you navigate the complexities and ensure success.

Did you find this article helpful? Discover more engaging insights and solutions from Legitt AI, including advanced sales enablement tools, an AI-powered proposal generator, and cutting-edge AI sales chatbot software. Contact us today to elevate your business with Legitt AI CRM software. Empower your business with Legitt AI!

FAQs on Fixed-Price Contract

What is a Fixed-Price Contract?

A Fixed-Price Contract is a legally binding agreement where the total cost of a project or service is set at a predetermined amount. The payment remains fixed regardless of time or resources used.

How does a Fixed-Price Contract work?

In a Fixed-Price Contract, both parties agree on a specific price for the defined scope of work. The contractor is responsible for completing the project within the agreed budget, bearing any additional costs that arise.

What are the advantages of a Fixed-Price Contract?

For buyers, the main benefits include predictable costs and reduced financial risk. For contractors, it offers a simpler payment structure and the incentive to work efficiently to maximize profits.

What are the risks of using a Fixed-Price Contract?

The primary risk for contractors is underestimating costs, which can lead to losses. For buyers, there may be a higher initial cost due to built-in risk premiums and limited flexibility to make changes.

When should you use a Fixed-Price Contract?

A Fixed-Price Contract is best for projects with a well-defined scope and predictable costs, such as construction, product development, or event planning.

Can a Fixed-Price Contract be adjusted?

In most cases, the price is fixed. However, contracts like Fixed-Price with Economic Price Adjustment (FPEPA) allow adjustments for inflation or rising material costs.

How do you draft a Fixed-Price Contract?

To draft a Fixed-Price Contract, you need to clearly define the scope of work, set a fixed price, establish milestone payments, and include risk and dispute resolution clauses.

How does Legitt AI help with Fixed-Price Contracts?

Legitt AI provides tools for automated contract drafting, AI-powered reviews, and risk analysis, ensuring your contracts are accurate, compliant, and well-structured.

What’s the difference between a Fixed-Price Contract and a Time and Materials Contract?

A Fixed-Price Contract has a set cost regardless of time or resources used, while a Time and Materials Contract is based on actual hours worked and materials used, offering more flexibility for evolving projects.