When borrowing or lending money, whether it’s between individuals or businesses, the terms of the loan must be clearly documented. Two common legal instruments used for this purpose are promissory notes and loan agreements. While both serve to formalize the loan process and outline repayment expectations, they differ in complexity, enforceability, and use cases. Understanding these differences is crucial for lenders and borrowers alike, ensuring that each party is adequately protected and aware of their obligations.

This article explores the nuances between promissory notes and loan agreements, outlining their respective definitions, key features, legal implications, and typical use cases.

Read More: How to Write a Contract

What is a Promissory Note?

A promissory note is a written, unconditional promise by one party (the maker or issuer) to pay a specific sum of money to another party (the payee or holder) either on demand or at a future date. Promissory notes are simple in form, and they typically do not involve complex terms or conditions. The note merely serves as evidence of debt and a repayment commitment.

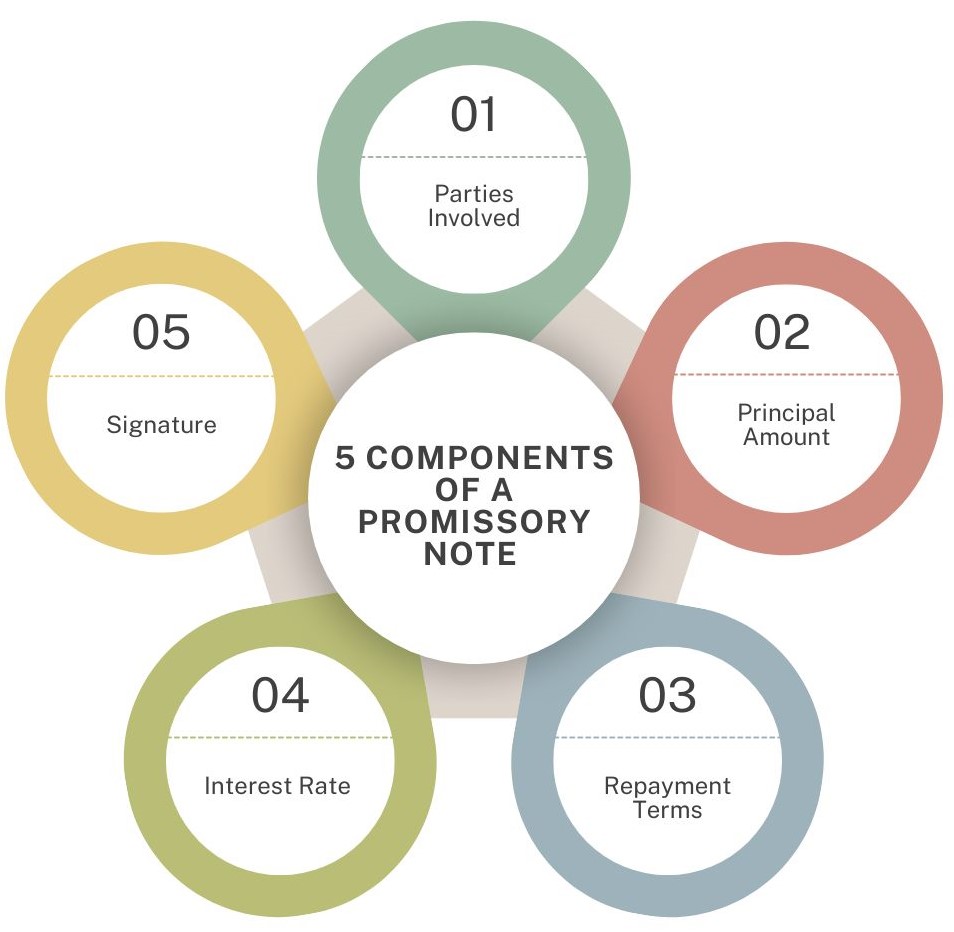

Key Elements of a Promissory Note:

- Parties Involved: The borrower (issuer) and the lender (payee).

- Principal Amount: The original sum of money borrowed, which must be repaid.

- Repayment Terms: Whether the debt is payable on demand or by a specific due date.

- Interest Rate (Optional): The note may or may not specify an interest rate for the loan.

- Signature: The promissory note must be signed by the borrower to be valid.

Types of Promissory Notes:

- Unsecured Promissory Note: No collateral is provided by the borrower. The lender’s only recourse is legal action in the event of non-repayment.

- Secured Promissory Note: The borrower provides collateral as security for the loan. If the borrower defaults, the lender may seize the collateral to recover the debt.

Legal Enforceability of a Promissory Note:

Promissory notes are legally binding documents. In the event that the borrower defaults, the lender can take legal action to recover the owed amount. The simplicity of a promissory note makes it suitable for smaller loans or transactions where minimal terms are required.

Use Cases for Promissory Notes:

- Personal loans between friends or family members.

- Informal business loans.

- Short-term loans or small sums of money.

- Loans where the borrower and lender have a high level of trust, and detailed terms are not necessary.

What is a Loan Agreement?

A loan agreement is a more detailed, formal contract that outlines the terms and conditions of a loan between two parties. It not only includes the promise to repay but also stipulates a wide range of additional terms, such as payment schedules, interest rates, default provisions, and borrower obligations. Loan agreements are comprehensive and are typically used for larger sums or more formal transactions.

Key Elements of a Loan Agreement:

- Parties Involved: The lender and the borrower, both of whom are identified clearly, often with detailed information about their roles.

- Loan Amount: The total sum of money borrowed.

- Repayment Schedule: Specific timelines for repayment, including the frequency of payments (e.g., monthly, quarterly, or annually).

- Interest Rate: The rate at which the loan accrues interest, whether fixed or variable.

- Collateral (Optional): Any assets that are pledged by the borrower as security for the loan.

- Loan Covenants: These are conditions placed on the borrower, such as maintaining certain financial metrics or avoiding other debt.

- Default Clauses: Provisions that define what constitutes a default and the actions that the lender may take in response, such as accelerating the loan or pursuing legal remedies.

- Signatures: Both parties typically sign the loan agreement to indicate consent to the terms.

Legal Enforceability of a Loan Agreement:

Loan agreements are more robust from a legal standpoint than promissory notes because they cover a wide range of scenarios, including contingencies and default conditions. They provide both parties with clear expectations and protections, ensuring that the lender has several legal avenues to recover their funds in the event of non-repayment.

Use Cases for Loan Agreements:

- Loans between businesses or individuals where a larger amount of money is involved.

- Mortgages, vehicle loans, and business loans.

- Loans that require formal collateral.

- Transactions where a lender and borrower need a structured agreement outlining all terms and conditions of the loan.

Key Differences Between Promissory Notes and Loan Agreements

1. Complexity

A promissory note is a straightforward document that is often only a few pages long. It includes basic information such as the loan amount, repayment date, and the borrower’s signature. Loan agreements, on the other hand, are detailed and complex contracts that contain numerous clauses and provisions. They address not only repayment terms but also contingencies, borrower obligations, and default conditions.

2. Formality

Promissory notes are often used in informal settings, such as loans between friends or family members, or small business loans where the relationship between the borrower and lender is based on trust. Loan agreements are formal contracts used in situations where a high level of detail and protection is required. These agreements are typically drafted by lawyers and used for substantial amounts of money or complex financial arrangements.

3. Collateral Requirements

While promissory notes can be either secured or unsecured, they typically do not include detailed provisions for collateral. If a promissory note is secured, the collateral agreement is often documented separately. Loan agreements, on the other hand, frequently include collateral clauses within the document itself. These provisions specify what assets are pledged as security for the loan and outline the lender’s rights to seize those assets if the borrower defaults.

4. Repayment Structure

A promissory note may or may not specify a detailed repayment schedule. It could simply state that the borrower promises to repay the loan either on demand or by a specified date. In contrast, a loan agreement always includes a clear repayment schedule, outlining the amount and frequency of payments over the loan term.

5. Legal Protection

Loan agreements provide more comprehensive legal protection to both parties compared to promissory notes. They include clauses that address potential disputes, default situations, and remedies for non-payment. Promissory notes, while legally binding, offer fewer protections and options for lenders in case of default. Loan agreements can include provisions such as arbitration clauses, late fees, and specific conditions for loan acceleration, providing more legal recourse for lenders.

6. Interest Rates

While both promissory notes and loan agreements can specify interest rates, loan agreements typically have more detailed provisions around interest. A loan agreement might specify whether the interest rate is fixed or variable, how interest is calculated, and how it changes over time. Promissory notes may include an interest rate, but it is often simpler and less detailed.

7. Use of Third Parties

Loan agreements often involve third parties, such as lawyers, financial advisors, or banks, in drafting and executing the contract. These third parties ensure that the agreement complies with local laws and protects the interests of both parties. Promissory notes are usually created and signed between the borrower and lender without third-party involvement.

Read More: How to Create a Security Agreement

When to Use a Promissory Note

Given its simplicity, a promissory note is ideal for smaller, less formal transactions where the borrower and lender trust each other. These scenarios typically include:

- Personal Loans: Borrowing money from friends or family members where both parties expect the transaction to be straightforward.

- Small Business Loans: For small, short-term loans between businesses or individuals, a promissory note can suffice, especially if the amount is not large.

- Purchase of Goods on Credit: Sometimes, a promissory note can be used when goods are sold on credit, and the buyer needs time to make full payment.

In these cases, the parties usually prefer simplicity over the added protection that a loan agreement offers.

Read More: Shareholder Loan Agreement

When to Use a Loan Agreement

Loan agreements are more appropriate for larger or more complex transactions where there is a need for a comprehensive and legally enforceable document. Common use cases include:

- Business Loans: When a business takes a loan from a financial institution or another business, a loan agreement is essential. These agreements ensure that the terms of the loan are clear and enforceable, protecting both the lender and the borrower.

- Mortgages: Real estate loans involve large sums of money, and lenders need to ensure that they have legal recourse in case the borrower defaults. Mortgage loan agreements include collateral clauses that protect the lender’s interest in the property.

- Long-Term Loans: When the repayment period spans several years, a loan agreement ensures that all terms are laid out in advance, reducing the chances of future disputes.

- Loans with Collateral: If the loan requires collateral, a loan agreement can specify the type of collateral, the conditions under which it can be seized, and the steps the lender can take if the borrower defaults.

Legal Considerations for Promissory Notes and Loan Agreements

Enforceability

Both promissory notes and loan agreements are legally binding documents. However, the enforceability of each depends on the jurisdiction and the specific terms included in the contract. Courts generally enforce loan agreements more strictly because of their comprehensive nature. If the borrower defaults, a lender with a well-drafted loan agreement will have more avenues for recourse than a lender with a simple promissory note.

Governing Law

For both types of documents, it’s essential to specify the governing law. This clause identifies the jurisdiction whose laws will govern the agreement. For example, if the parties are located in different states or countries, they must decide which jurisdiction’s laws will apply in the event of a dispute.

Drafting Considerations

When drafting either a promissory note or a loan agreement, it’s crucial to ensure clarity in the terms. Ambiguities can lead to disputes and make it difficult to enforce the document. If the loan is substantial or involves complex terms, it’s advisable to have a legal professional draft the loan agreement to ensure that it protects the lender’s interests and complies with applicable laws.

Read More: How to Write a Contract

Conclusion

Both promissory notes and loan agreements serve the essential purpose of formalizing a loan, but they differ significantly in their complexity, formality, and use cases. A promissory note is simple and ideal for smaller, less formal loans, while a loan agreement is more detailed and appropriate for large, complex loans that require extensive terms and protections. Understanding these differences helps lenders and borrowers choose the right instrument for their situation, ensuring that both parties are adequately protected and that the loan terms are clearly defined.

While both documents are legally binding, loan agreements offer more comprehensive legal protection, making them preferable for formal, long-term, or secured loans. Conversely, promissory notes are simpler and easier to execute, making them suitable for more informal, short-term lending arrangements.

Did you find this article worthwhile? More engaging blogs and products about smart contracts on the blockchain, contract management software, and electronic signatures can be found in the Legitt AI. You may also contact Legitt to hire the best contract lifecycle management services and solutions, along with free contract templates.

FAQs on Promissory Note vs Loan Agreement

What is the main difference between a promissory note and a loan agreement?

A promissory note is a simple document that records the borrower’s promise to repay a specific amount of money to the lender, often without detailed terms. A loan agreement is more comprehensive and includes detailed terms and conditions, such as repayment schedules, interest rates, default clauses, and collateral requirements.

When should I use a promissory note instead of a loan agreement?

A promissory note is typically used for smaller, informal loans between individuals or businesses where the terms of the loan are straightforward. It’s best suited for situations where the lender and borrower have a high level of trust, such as loans between friends, family members, or small business transactions.

Is a promissory note legally binding?

Yes, a promissory note is legally binding as long as it includes the borrower’s signature and clearly states the amount to be repaid. However, it is less detailed than a loan agreement, which may offer more legal protection in case of a dispute or default.

Can a promissory note include interest, and how is it calculated?

Yes, a promissory note can include interest. The interest rate is typically specified in the document, and it can be either a fixed rate or a variable rate. The calculation method is usually straightforward, though not as detailed as the provisions in a loan agreement.

What is the purpose of a loan agreement?

A loan agreement provides a comprehensive framework for larger, more complex loans. It outlines detailed repayment terms, interest rates, borrower obligations, collateral requirements, and default conditions, offering legal protection for both parties involved in the loan transaction.

Can I secure a loan with collateral using a promissory note?

Yes, promissory notes can be secured with collateral, but this is less common than with loan agreements. When a promissory note is secured, the collateral agreement may be documented separately. Loan agreements often integrate collateral terms directly into the document, offering a clearer legal recourse for lenders.

Which document offers better protection in case of a loan default?

A loan agreement provides better protection in case of default because it includes detailed provisions for what happens if the borrower fails to repay the loan. This can include acceleration clauses, late fees, and other penalties. A promissory note, while legally binding, is typically less comprehensive in its default provisions.

Do I need a lawyer to draft a loan agreement or a promissory note?

For small, informal loans, you may not need a lawyer to draft a promissory note. However, for larger loans or complex arrangements, it is advisable to have a lawyer draft or review a loan agreement to ensure it includes all necessary legal protections and complies with local laws.

Can a loan agreement or promissory note be enforced in court?

Yes, both loan agreements and promissory notes can be enforced in court if the borrower defaults. However, because loan agreements are more detailed and comprehensive, they may provide stronger legal standing and better protection in the event of a legal dispute.

What should I do if the borrower defaults on a promissory note or loan agreement?

If a borrower defaults on a promissory note or loan agreement, the lender can take legal action to recover the debt. In the case of a loan agreement, the terms of default and remedies are typically outlined in detail, providing clear steps for the lender to follow. With a promissory note, the lender may need to file a lawsuit to enforce the repayment terms.