Contract Lifecycle Management

Featured

CONTRACT VISIBILITY GAP: WHY MOST ORGANIZATIONS MISS HIDDEN RISKS IN THEIR AGREEMENTS

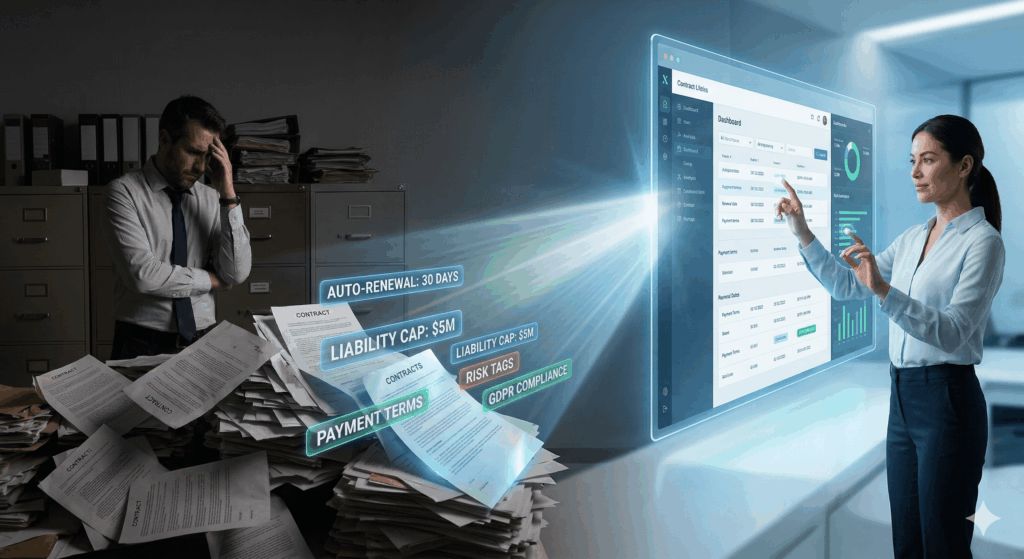

Contracts are around us in the business world. The sales team signs agreements with customers. The procurement team manages contracts…

March 24, 2026 · 8 min read